Why Oil Prices Aren’t Soaring Despite the Biggest Energy Crisis

The Global Energy Crisis: A New Era of Uncertainty

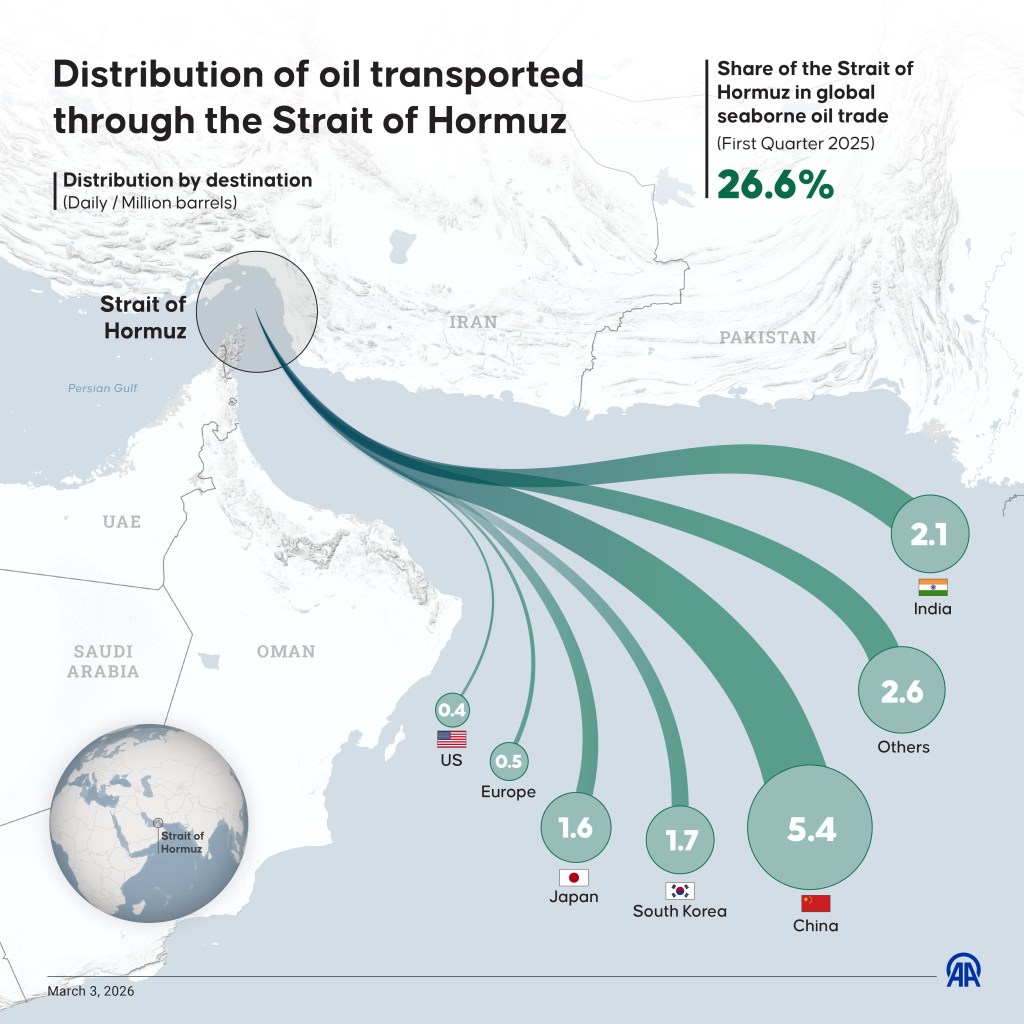

The ongoing conflict in Iran has triggered what many experts are calling the most significant energy supply shock in history. At the heart of this crisis lies the Strait of Hormuz, a critical chokepoint through which 20% of global oil and liquefied natural gas flows daily. With this vital route effectively closed off, the world is witnessing an unprecedented disruption in energy markets.

Despite the severity of the situation, global oil prices have not yet reached the record highs that one might expect. As of now, the U.S. benchmark for oil is hovering near $100 per barrel—an increase of 70% since the beginning of the year. However, analysts argue that the extent of the disruption should theoretically push prices to $150 per barrel or higher, especially considering that Israel and Iran have begun targeting gas fields and infrastructure that could lead to long-lasting damage across the Gulf region.

So why hasn’t this happened yet?

Energy analysts point to several key factors that are currently keeping prices from spiking even further:

- Reduced Reliance on Middle Eastern Oil: Many countries, including the U.S. and much of Europe, are less dependent on Middle Eastern oil than they have been in decades. This is due to increased domestic production and a growing shift toward renewable energy sources.

- Emergency Oil Supplies: There are greater emergency oil reserves globally compared to the 1970s, when the Arab oil embargo led to the creation of the U.S. Strategic Petroleum Reserve.

- Optimism About a Short War: Oil traders remain hopeful that the conflict will be short-lived. They believe that Saudi Arabia, Iraq, and the United Arab Emirates will continue to reroute their exports to provide temporary buffers until the Strait of Hormuz is reopened. Additionally, Iran is still exporting some of its oil, allowing select tankers to pass through, such as those heading to India.

- Uneven Impact: The war is most severely affecting countries like Pakistan, Bangladesh, and parts of Southeast Asia, which rely heavily on Middle Eastern oil and gas supplies.

The U.S. Is Less Affected—For Now

While the U.S. is not immune to the effects of the crisis, it is relatively insulated compared to other regions. As of March 18, the average price for a gallon of regular unleaded in the U.S. was $3.86, up $1.13 from the January low. That’s a 40% increase, but still significantly lower than in Europe.

According to Jim Wicklund, a veteran oil analyst and managing director at PPHB energy investment firm, “Southeast Asia is getting nailed by this, but the reality is, in our part of the world, nobody even knows where Indonesia is.” He added, “As consumers in the U.S., we’re horribly spoiled. There’s no panic anywhere. Yeah, my gasoline prices are $1 higher, which is still [nearly] $4 cheaper than Europe.”

In the U.S., only about 3% of oil consumption comes from the Middle East—the lowest level since the Arab oil embargo of the 1970s. The majority of U.S. oil consumption is met by domestic production, with Canada providing most of the imports. Mexico follows as the next major supplier.

However, the U.S. has taken action to mitigate potential shortages. Beginning in late March, the country started releasing 172 million barrels of oil from its strategic reserves over a few months. This move highlights the interconnected nature of global energy markets.

The Risk of Escalation

Israel’s recent attack on Iran’s South Pars gas field has prompted Iran to threaten retaliatory strikes against the refineries and gas fields of its neighbors. Already, the UAE has halted operations at its Shah gas field following Iranian drone attacks. The UAE’s alternative route, the Fujairah oil port, has also been targeted.

If Iran successfully attacks major oilfields in neighboring countries, the “higher for longer” mentality of oil prices will likely take hold, according to Dan Pickering, founder of Pickering Energy Partners. This is because long-term infrastructure damage would reduce global supply, pushing prices higher. The stock market could react in real time, with the U.S. oil benchmark potentially rising to $130 per barrel within a couple of weeks.

Derek Bunn, an energy economist at the London Business School, agrees. “If things do not get resolved politically fairly soon, then these longer-term effects will start to bite,” he said. “And it may not be that long.”

The Potential for Even Higher Prices

Andrew Harbourne, senior oil analyst at Wood Mackenzie, noted that while global benchmarks are trading near $100, the prices for Middle Eastern barrels escaping the Persian Gulf are already closer to $150 per barrel. If the Strait of Hormuz remains blocked for an extended period, Harbourne warns that global oil prices could converge at the higher levels observed so far and potentially exceed $200 per barrel.

Jim Wicklund sees the conflict as a matter of “politics and logistics” that must be resolved sooner rather than later. He pointed out that President Donald Trump is unlikely to want oil prices above $100 per barrel as the midterm elections approach in November.

“Everybody knows this can’t continue. Nobody knows how it ends. This is interrupting economic commerce for everyone in the world to the tune of billions of dollars a day,” Wicklund said.

The war’s impact extends beyond just fuel prices. It is causing sharp increases in the cost of aluminum, fertilizer, cooking oil, grains, sugar, petrochemicals, and helium. These rising costs are quickly trickling down into inflation for food, electronics, pharmaceuticals, and most consumer goods.

“But that’s the whole attitude of the market these days: ‘We’ll see. I hope it doesn’t take too long,’” Wicklund said.